Fintech

For many years, banks have had the power to send money across the world. Whether you're paying a supplier in Asia, a contractor in Europe, or an employer in Africa, the process has always been the same. Open a bank account, start a wire transfer, wait for SWIFT, pay extra fees for exchanging money, then keep fingers crossed and hope that the transaction doesn’t get blocked by rules.

By the route we grip, money is transformed. Businesses are currently global from day one and expect their money to move at internet speed—not banking speed. That’s where Endl's business account comes in: a stablecoin-powered business account that makes global payments instant, transparent, and compliant.

So how does Endl stack up against traditional banks?

Let's break it down by what matters most: fees, speed, and trust.

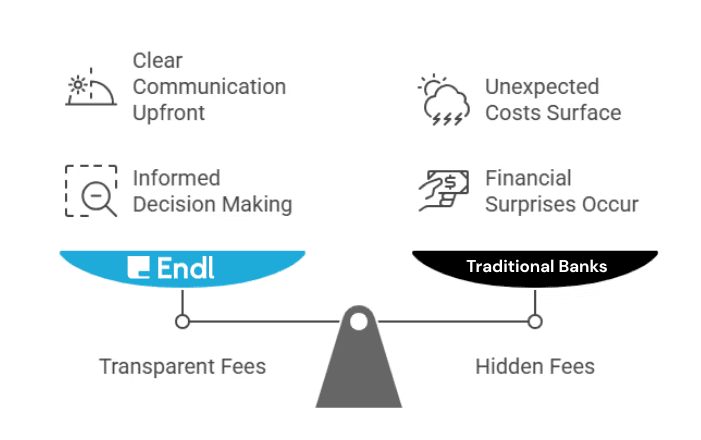

Fees: Transparent vs. Hidden

How Banks Handle Fees

If you've ever sent a wire transfer, you know the frustration: High fixed fees ($20–$50 per wire). Intermediary bank charges (sometimes deducted along the way). Hidden FX spreads (your bank's exchange rate is often 2–4% worse than the market rate), according to Forbes.

A simple $10,000 transfer to pay an overseas vendor can incur hundreds of dollars in hidden fees. Multiply that by dozens of payments per month, and the losses are staggering. Banks thrive on opacity. You rarely know the exact cost until after the money leaves your account.

Endl’s Approach to Lowering Business Payment Fees

At Endl, fees are transparent and fair: Low transaction fees (often a fraction of bank wires).

Live FX rates (no hidden spreads, you see the real-time conversion before you hit send). Stablecoin option (bypass FX altogether by paying in USDC or USDT).

Example: Paying a supplier in Berlin €20,000 via a traditional bank might incur fees of over $200, plus a poor exchange rate. With Endl, you'd see the real FX rate upfront, pay a fraction of the cost, and your supplier gets the full amount in minutes.

Verdict on Fees: Endl wins.

Banks make money by keeping you in the dark.

Endl makes money move cheaper, faster, and with total transparency.

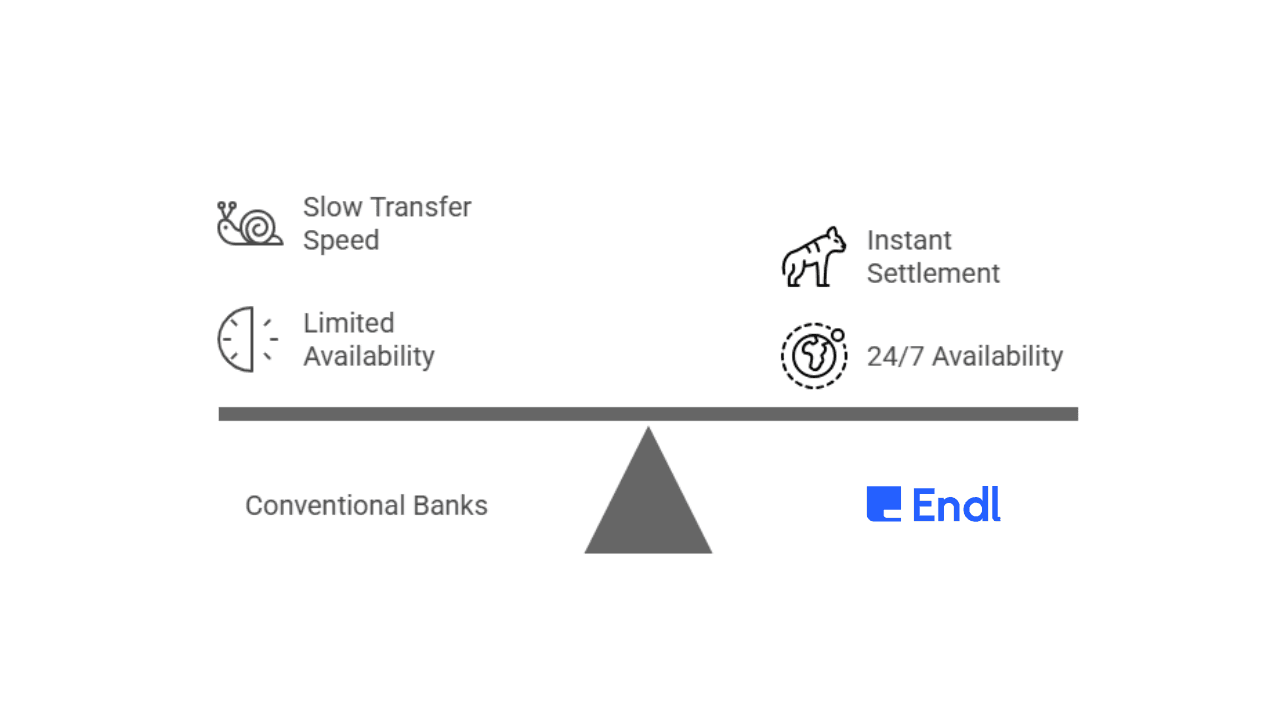

Speed: Days vs. Minutes

How Banks Handle Speed

Conventional banks still run on infrastructure built decades ago. SWIFT transfers take 2–5 business days. Payments stall over weekends and holidays. Cut-off times mean if you miss 4 p.m. Friday, your money won’t move until Monday. Even domestic transfers can take hours to clear. Global payments are even slower, thanks to correspondent banks passing funds between multiple middlemen.

How Endl Achieves Near-Instant Settlement for Cross-Border Payments

Endl runs on blockchain rails + traditional networks, giving you the best of both worlds: Instant settlement in stablecoins (USDC, USDT). Near-instant fiat payouts to local bank accounts worldwide. 24/7/365 availability (no banking hours, no waiting for Monday).

Example: A startup in New York needs to pay its developer in Kenya on a Saturday night. With a bank, the transfer wouldn’t even start until Monday, and the developer might see funds on Wednesday. With Endl, the payout lands in USDT in minutes or in KES via a local bank by the next morning.

Verdict on Speed: Endl wins.

Banks operate on banking hours.

Endl operates on your hours.

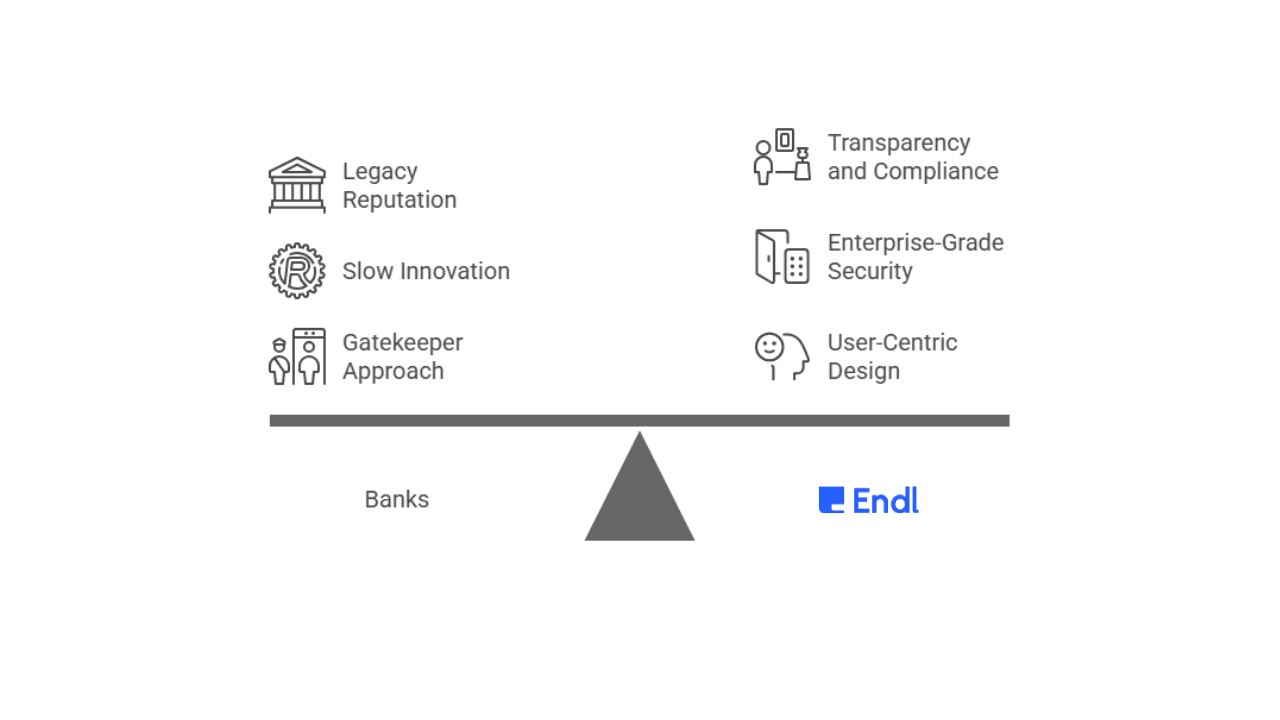

How Banks Handle Trust

Banks have the advantage of a legacy reputation. For centuries, they’ve been seen as the “safe” option. But: They are often slow to innovate, relying on outdated systems. Their compliance processes are opaque and inconsistent. They’ve faced repeated scandals around hidden fees, fraud, and mismanagement. While banks are trusted, they aren’t necessarily transparent.

How Endl Handles Trust

Endl was built for the modern world, where trust is about transparency + compliance + security.

Compliant by design: We adhere to global KYC/AML standards and partner with regulated financial institutions.

Stable and transparent: Funds held in fully backed stablecoins like USDC and USDT.

Enterprise-grade security: Fraud monitoring, anomaly detection, 99.9% uptime.

Future-ready: No gambling with customer funds, no risky speculation—just stable, secure money movement.

And unlike banks that sometimes feel like gatekeepers, Endl is designed to be your partner: approachable, user-centric, and transparent.

Verdict on Trust: Tie (with a twist): Banks win on legacy reputation. Endl wins on transparency, compliance, and future-readiness. For a modern global business, Endl offers trust without friction.

Endl vs. Conventional Banks Side by Side

Fees

Banks: High, unpredictable, hidden FX spreads.

Endl: Transparent, low-cost, live rates.

Speed

Banks: 2–5 days, limited to banking hours, cut-off times.

Endl: Minutes, always-on, powered by blockchain rails (24/7/365).

Trust

Banks: Legacy reputation, but opaque compliance processes.

Endl: Compliant by design, transparent, enterprise-grade secure.

Currencies

Banks: Limited support, slow FX conversions.

Endl: Multi-currency + stablecoins (USD, EUR, GBP, USDC, USDT).

Global Reach

Banks: Limited coverage, costly corridors.

Endl: 200+ countries supported with both fiat & stablecoin rails.

Ease of Use

Banks: Clunky portals, manual processing.

Endl: Intuitive dashboard, no-code payouts, API for automation.

Innovation

Banks: Slow-moving, outdated systems.

Endl: Future-ready finance, yield options, programmable APIs.

Real-World Example: Paying Global Teams

Scenario 1: Using a Bank

A startup needs to pay 50 remote employees across 12 countries.

The CFO spends hours preparing wire transfers.

Pays thousands in cumulative fees.

Waits days for confirmation.

Scenario 2: Using Endl

Uploads one payout file.

Clicks once.

All employees get funds in their preferred currencies (fiat or stablecoin) within minutes.

Why Banks Still Have a Role: And Why Endl Is Different

We won’t pretend banks are obsolete.

They still play a critical role in global business banking:

Safeguarding deposits.

Providing lending services.

Offering regulated stability.

But when it comes to cross-border payments and international money movement, they simply can’t keep up. Endl doesn’t replace banks entirely; we complement them.

Think of Endl as the bridge between the reliability of traditional finance and the agility of the stablecoin banking ecosystem—bringing the best of both worlds through faster, transparent, and compliant global transactions.

Final Verdict: The Future Belongs to Speed, Transparency, and Trust

On fees, Endl wins: transparent, lower, fair.

On speed, Endl wins: minutes, not days.

On trust, it’s close—banks have legacy clout, but Endl is building modern trust through compliance, stability, and transparency.

For modern businesses, especially those operating globally, the choice is clear.

Banks might be safe, but they’re slow and expensive. Endl is safe, and it’s fast, transparent, and built for the future. Because when your money moves freely, your business does too.

Citations:

SWIFT Official Site: https://www.swift.com/

Circle – About USDC Stablecoin: https://www.circle.com/

Forbes – Why Stablecoins Are Changing Global Payments: https://www.forbes.com/

IMF – The Rise of Digital Money: https://www.imf.org/en/Publications/fandd/issues/2019/09/the-rise-of-digital-money-gopinath

CoinDesk – How Stablecoins Power the Next Generation of Cross-Border Payments: https://www.coindesk.com/

FAQs:

Q1: What makes Endl different from a traditional bank?

A: Endl offers instant, 24/7 global payments using stablecoins, transparent fees, and real-time FX rates—unlike traditional banks that rely on slow and costly systems.

Q2: Is Endl safe to use for business payments?

A: Yes, Endl is compliant with global KYC/AML standards, partners with regulated financial institutions, and uses enterprise-grade security to keep funds safe.

Q3: Can Endl replace my business bank account?

A: Endl complements banks—it’s a modern bridge that gives you global reach, stablecoin flexibility, and faster transfers

Q4: How does Endl help with international money transfers?

A: Endl simplifies cross-border payments by combining blockchain rails and traditional networks. You can send or receive money in multiple currencies or stablecoins (USDC, USDT) instantly—without delays, hidden FX costs, or intermediaries.